Plansponsor.com annually publishes a very insightful participant survey. I’ve extracted a few impactful findings I wanted to share. I’ve included the complete survey weblink below to review.

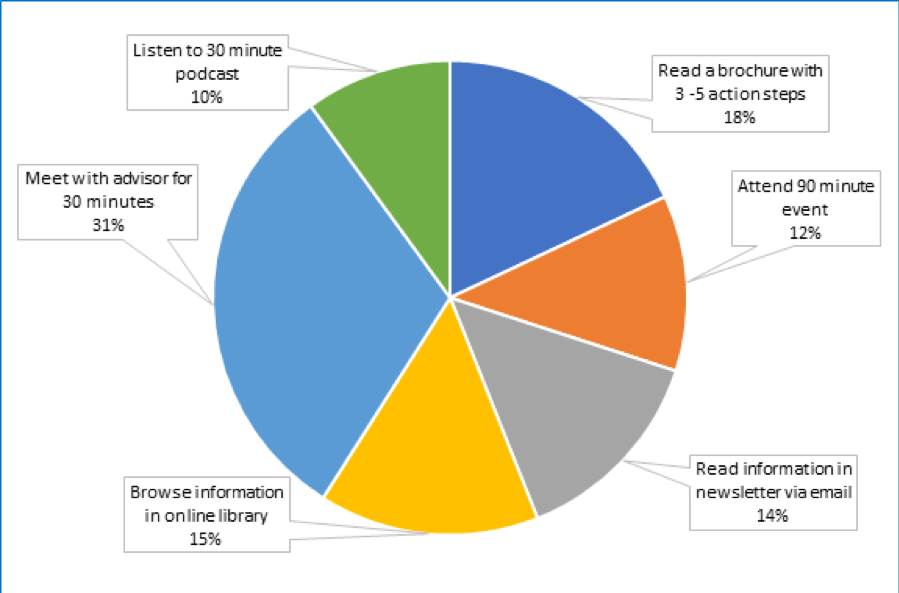

This 1st chart shows how plan participants would prefer to get information about financial wellness. Does your company provide financial wellness using any of these methods? Does your company offer 30-minute meetings with plan advisors? Do you survey your employee base to ask how they’d like to learn about financial wellness?

How Would You Prefer to Receive Information on Financial Wellness?

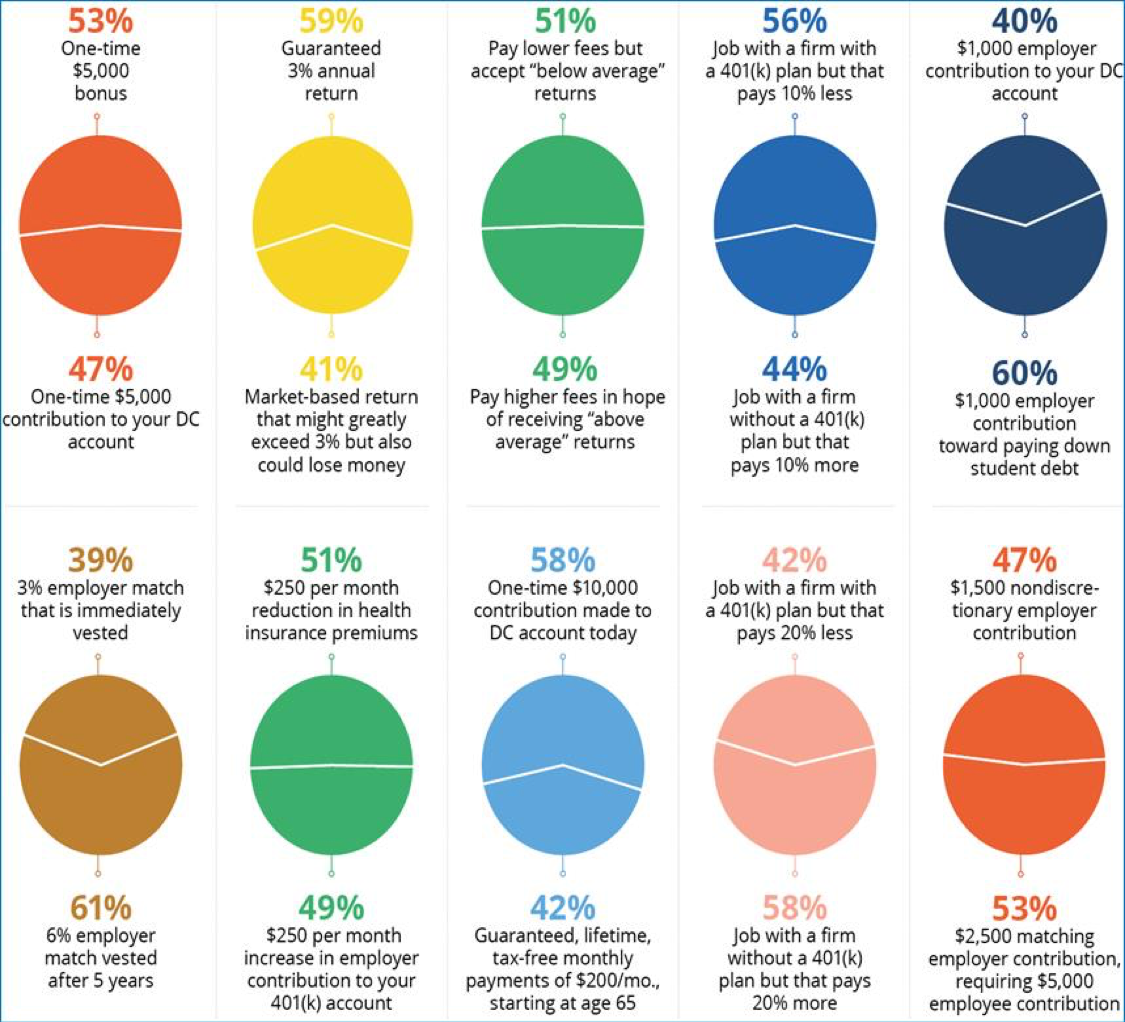

This 2nd chart is a combination of trade-off scenarios. Respondents were presented with two options for each of the following scenarios and selected their preference. What benefits does your current plan offer and are they important to your employees? Do you survey your employees to find out?

Trade-offs – which option do you prefer?

Plansponsor.com adds the following feedback about how providers can improve.

The defined contribution (DC) industry has evolved since 2014, the year of our first PLANSPONSOR Participant Survey, but participants remain largely unchanged in how they value—and would trade off—employer benefits.

As a general rule, employees prefer benefits that deliver greater vs. quicker financial impact. For example, 61% of respondents prefer a 6% match that becomes vested after five years to a 3% match that is immediately vested. Similarly, a record 53% of respondents now prefer a $2,500 matching contribution to a $1,500 employer contribution that does not require that employees pay in. This perhaps reflects a growing acceptance by employees of their role in saving for retirement.

Further, our 2019 survey confirms that DC plans can help “attract and retain” employees—within limits. This year, 56% of respondents would choose an employer with a 401(k) but offering 10% less pay to one that offers 10% more pay without a plan. However, loyalty appears to have its limits, as that number drops to 42% when the pay gap is 20%.

When choices have no clear difference in value, employees lean toward shorter-term benefits. A slim majority (53%) would opt for a one-time $5,000 bonus over a one-time $5,000 contribution to a 401(k) account, while a more decisive 60% of those with student debt would opt for a $1,000 employer-sponsored student debt payment over a $1,000 contribution to a 401(k) account. —PlanSponsor.com

Here’s the hyperlink to the survey – https://www.plansponsor.com/research/2019-participant-survey/3/#Findings

As many of us have learned, incentives work. Understanding what is important to your employees and then providing what is possible in your benefits program can improve employee engagement and workplace satisfaction.

Contact Thoughtful Advisors to Understand What Is Possible.